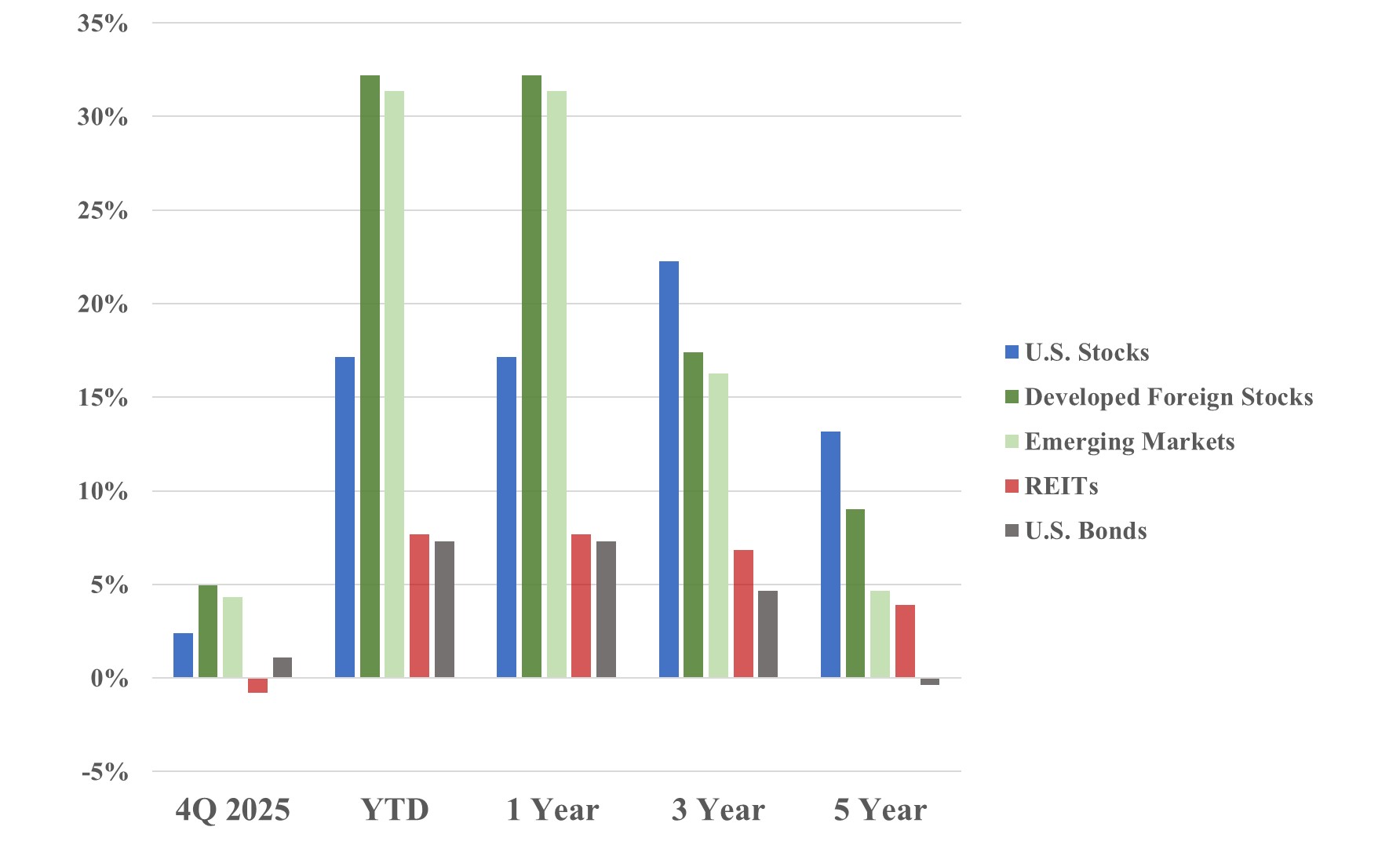

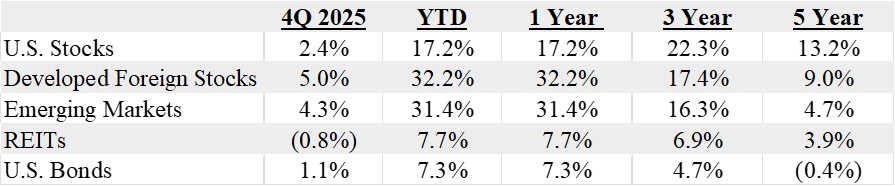

Market Review

The big story for the fourth quarter was continued strength from international stocks (in both relative and absolute terms). Developed and emerging market stock indices finished 2025 up >30% (vs. U.S. stocks up “only” 17% for the year) with help from a weakening U.S. dollar but also from a narrowing of the gap in relative valuation levels (with international stocks still trading below their historical average discount to U.S. stocks). We remain convinced that global diversification makes sense for long-term equity investors and that, over time, global economic growth will drive price appreciation for both domestic and international stocks.

REITs and bonds were both flattish for the fourth quarter but finished 2025 up 7-8% as interest rates trended lower. Note that trailing 5-year returns for both REITs (+4%) and bonds (flat) remain well below their long-term averages (+10% for REITs +5% for bonds) which could bode well for the next few years.

Index performance is provided as a benchmark. It is not illustrative of any particular investment. An investment cannot be made in an index. Past performance is not an indication of future results. Russell 3000 Index, MSCI World ex USA Index, MSCI EM Index, S&P Global REIT Index, US Aggregate Bond Index. Returns as of 12/31/2025.

Economic Review

[Keep in mind: the economic data usually lags a bit]

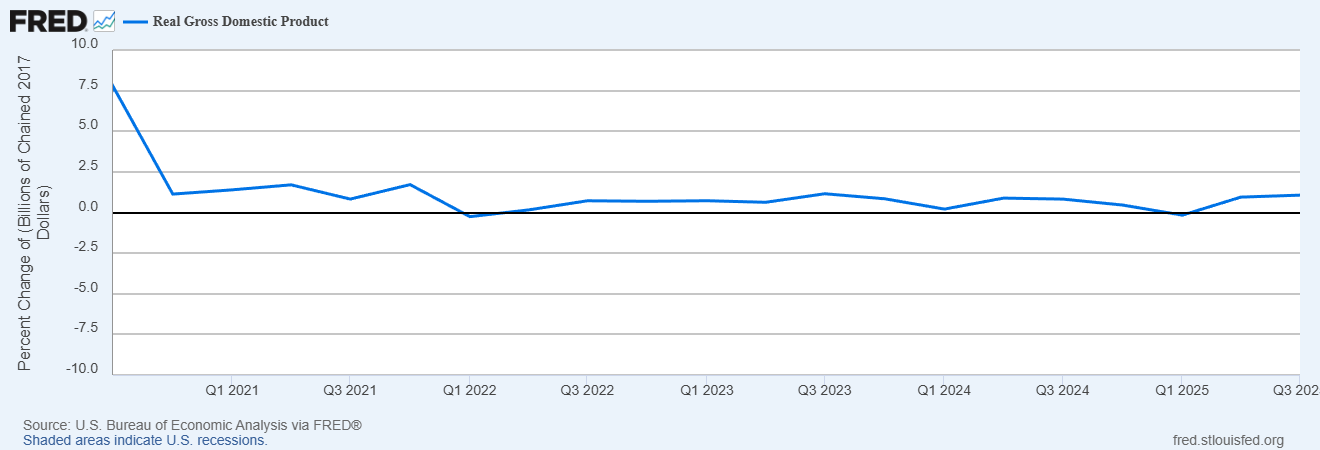

Real (inflation-adjusted) GDP growth accelerated further in Q3 (+4.3% annualized growth) driven by continued resilience in consumer spending with help from government spending and higher exports.

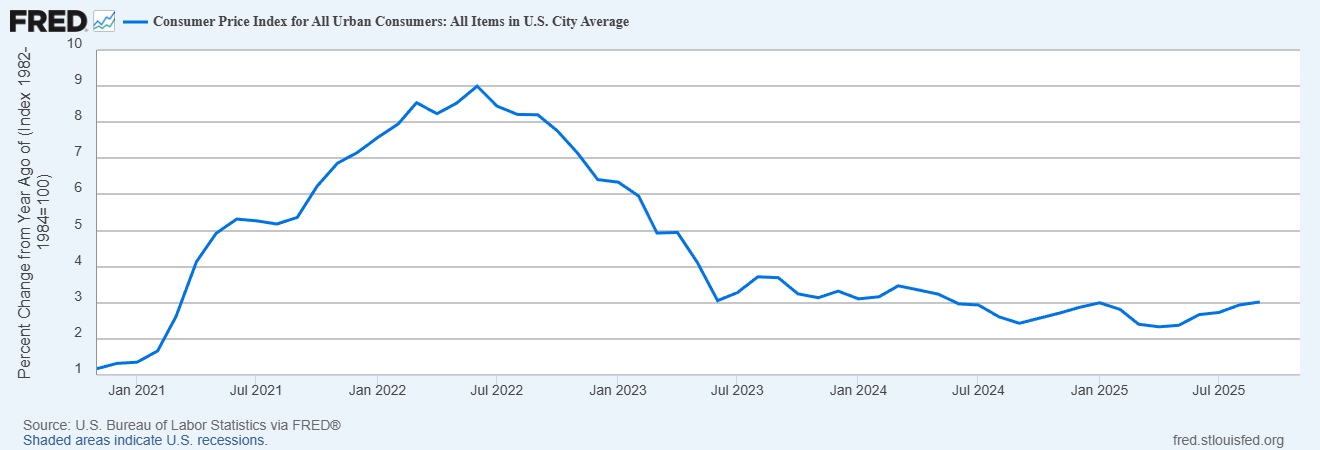

Inflation declined from +3.0% in September to +2.7% in November (note that the Fed’s graph above ends in September since October was not reported due to the government shutdown).

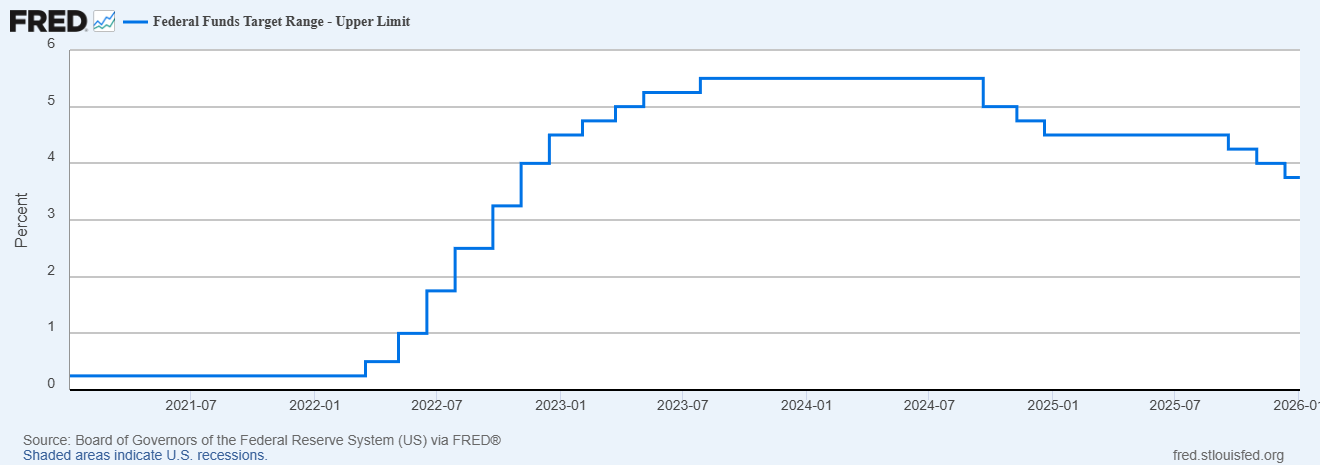

The Fed reduced the Federal Funds rate by another 0.50% during the fourth quarter to 3.75% and they also published estimates for the Federal Funds rate to decline further to 3.4%/3.1% at year-end 2026/2027.

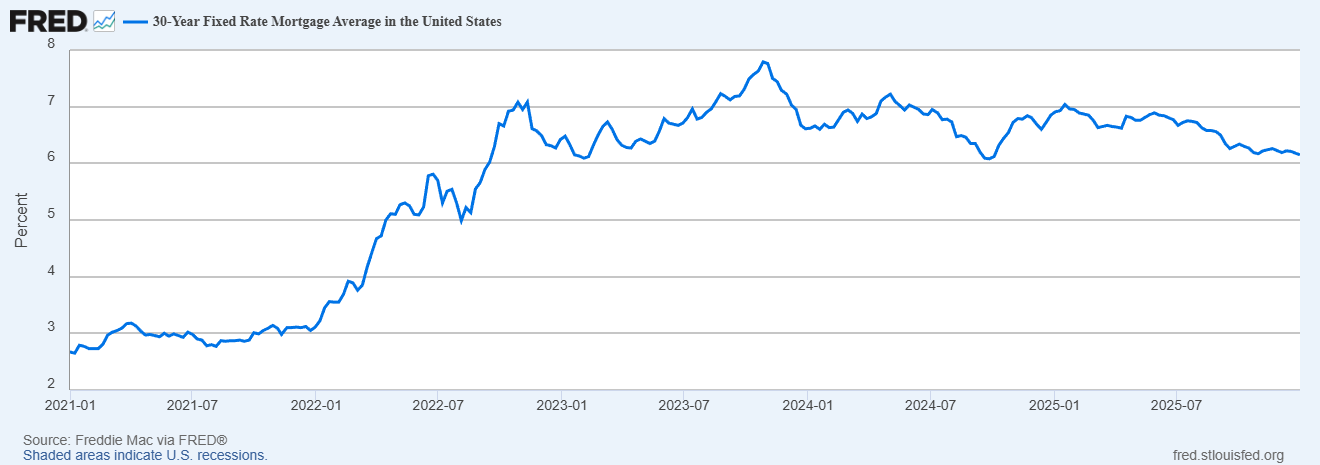

Mortgage rates continued to grind lower during the fourth quarter and reached 6.15% in December (down from 6.9% at the end of 2024).

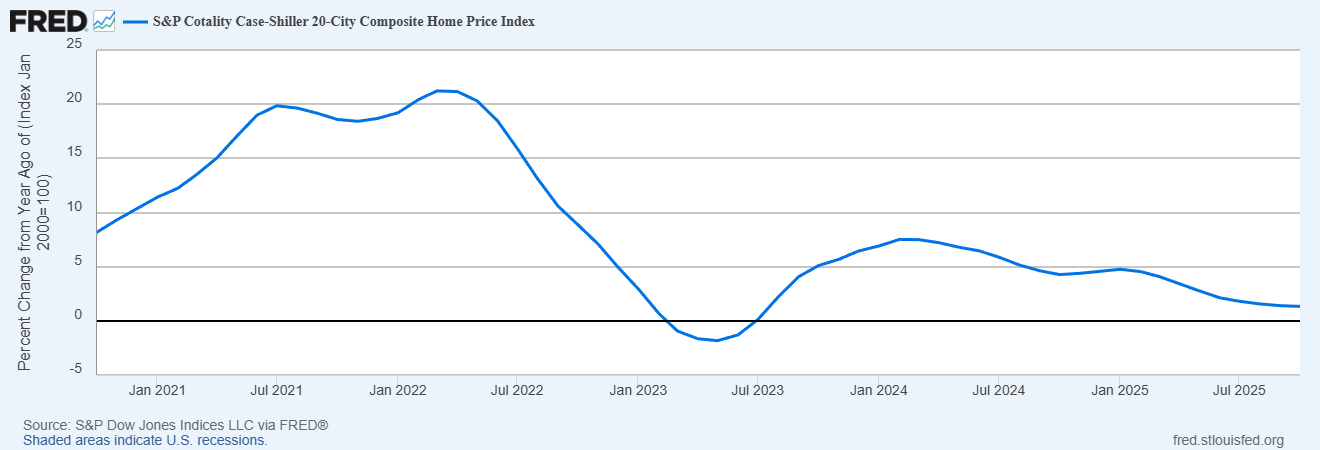

Home prices remained relatively stagnant in October (+1% higher than last year) with 16 of the 20 cities in the S&P 20-city index showing sequential price declines.

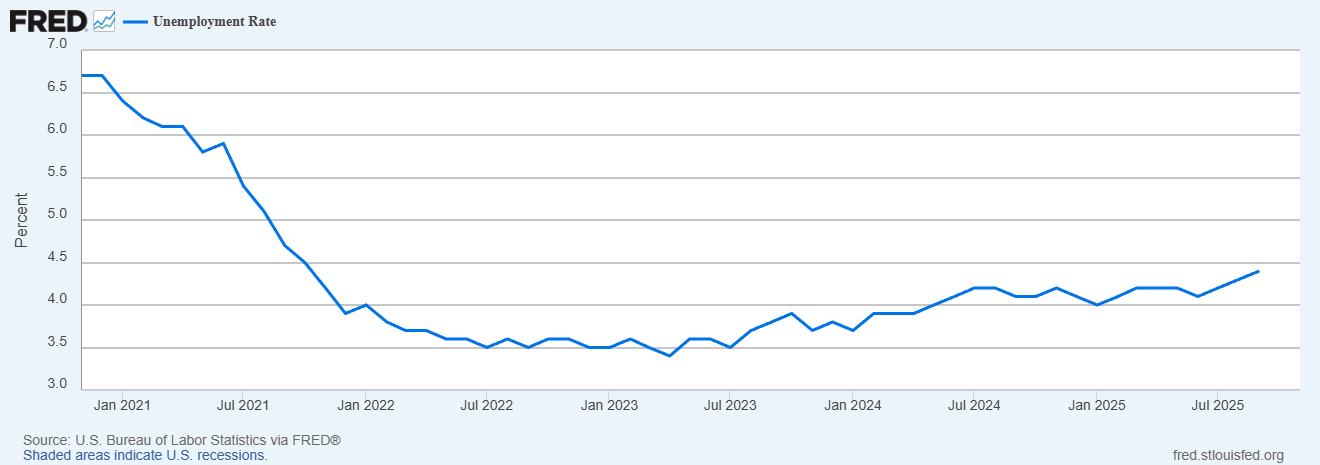

The unemployment rate continued the upward trend that we’ve seen since mid-2023, reaching 4.6% in November as the pace of hiring has remained slow across many sectors (again note that the Fed’s graph above does not show the November data point since October data was never released).

Tax, Legal, & Legislative Updates

- Social Security cost of living adjustment (COLA) will be a 2.8% increase for 2026.

- Contribution limits for retirement accounts were increased for 2026 by the IRS to $7,500 for IRA accounts (with additional $1,100 catch-up for those over 50).

- Contribution amounts for retirement plans: $24,500 for 401(k), 403(b), and governmental 457 plans.

- 401k catch-up limits age 50+ are now $7,500

- 401k catch-up limits ages 60-63 are now $11,250