A Flat-Fee Model for $5-25M Families

"The miracle of compounding returns is overwhelmed by the tyranny of compounding costs." - John C. Bogle

Birchwood's Fee: $24,000 per year, per household

We built a wealth management model specifically for affluent families who no longer believe percentage-based pricing makes sense.

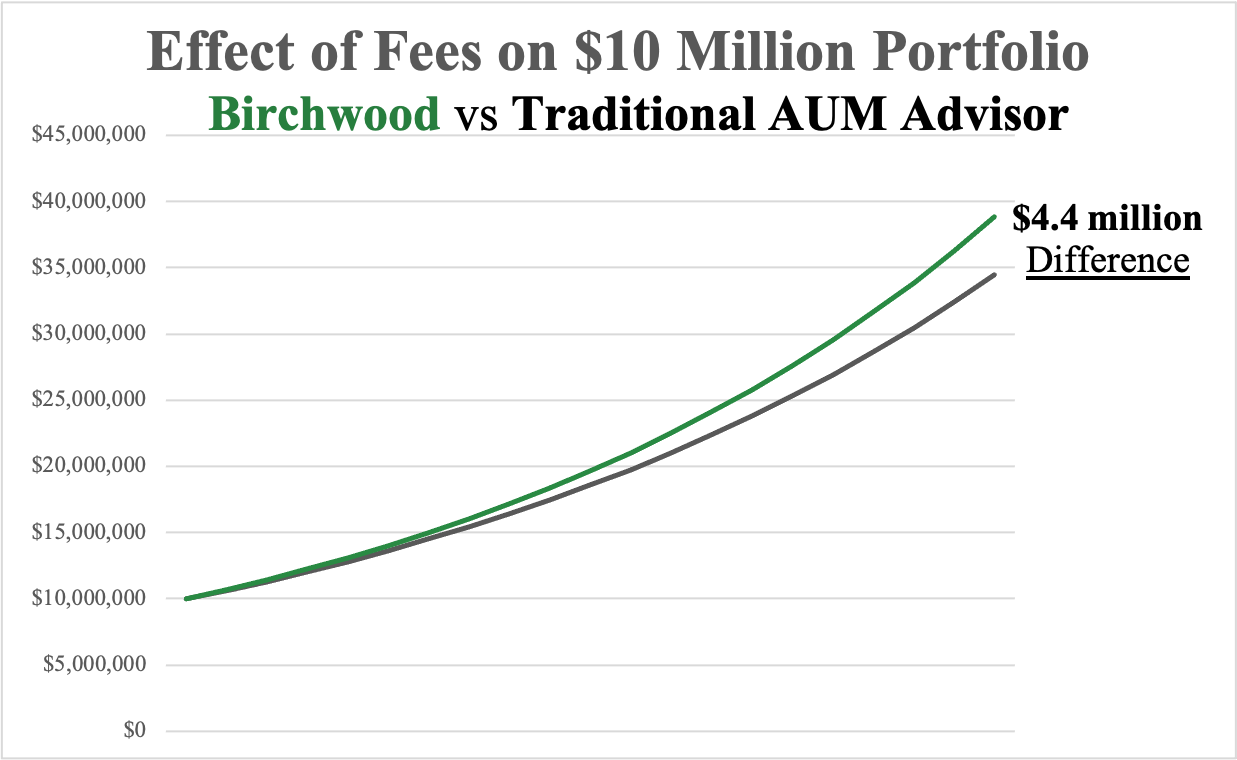

Chart shows the impact of fees on a $10,000,000 portfolio with an annualized return of 7% over a 20-year period. Assumes no contributions or distributions. AUM fees are 0.75%. Birchwood's fee is $24,000/yr and inflated at 2% annually for illustrative purposes only. The use of a 7% annualized return is in no way indicative of an actual return realized by a client. No guarantee of a return is implied or intended.

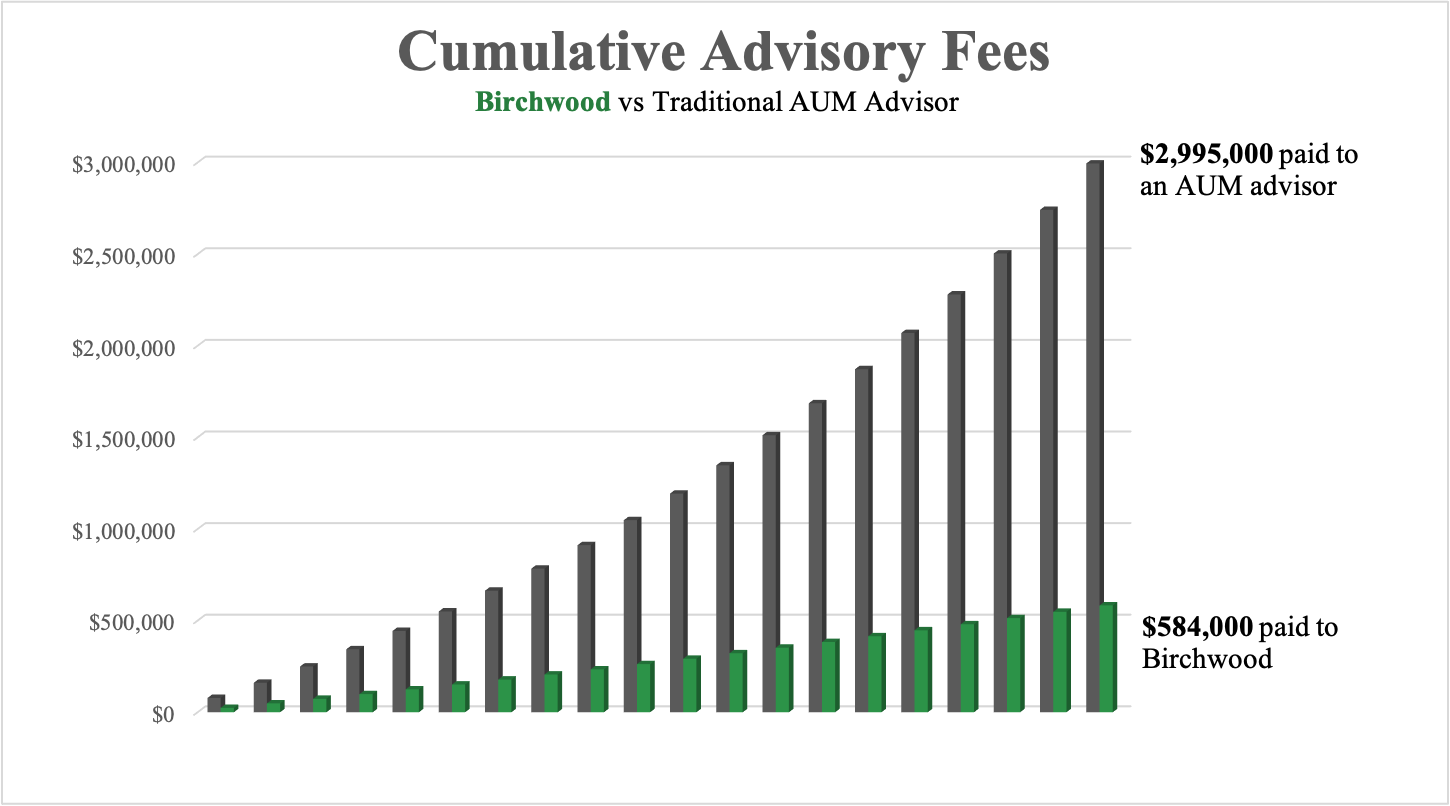

The chart shows the total (cumulative) advisory fees paid to Birchwood vs. a Traditional AUM advisor. Assumes $10,000,000 portfolio with an annualized return of 7% over a 20-year period. Assumes no contributions or distributions. AUM fees are 0.75%. Birchwood's fee is $24,000/yr and inflated at 2% annually for illustrative purposes only. The use of a 7% annualized return is in no way indicative of an actual return realized by a client. No guarantee of a return is implied or intended.

Why It Matters

Over the past few decades, the financial services industry has attempted to align itself more with clients by reducing conflicts of interest. We’ve seen a reduction in commission-based products and greater public education about who is a true fiduciary and who is not.

All of these are good things. Removing the incentive for brokers and advisors to churn clients accounts and creating greater consumer awareness about who is legally obligated to do what’s in client’s best interest leads to better outcomes for clients in general. But, stubbornly, the largest conflict of interest remains: fees for financial advice being based on assets under management (or AUM).

When firm revenue is derived directly from the amount of assets managed, it becomes exceedingly difficult (or impossible) to recommend a mortgage to be paid off or the rolling of an IRA back into an employer-sponsored 401(k) to prevent RMD’s by using money that is invested with the firm. There are many situations where taking investments out for some other purpose is in the best interest of the client, but not necessarily in the best interest of the firm.

Not only that, this widespread acceptance of assets under management has allowed for massive economies of scale to be inflicted on clients - taking earnings that are rightfully theirs and putting it in the pockets of brokerage firms and investment advisors. It does not cost a firm more to manage a $10,000,000 portfolio versus a $5,000,000 portfolio. If clients are receiving the same services, why should some pay more?

The truth is the majority of consumers who utilize financial advisors don’t know much about the service and what they are buying. They lack the power that an informed consumer should have.

We set out to change this by asking two basic questions:

-

How would I want to be charged if I was hiring an advisor?

-

What does an advisor actually do and what is that actually worth?

As a flat-fee financial advisor, Birchwood Capital has built a fee structure around the services we provide for the type of clients we serve. This flat annual fee is based on our costs and reasonable compensation for a professional service provider. We believe this is a more appropriate fee structure and that clients will greatly benefit from it.