The first quarter saw a 9% drawdown in U.S. stocks driven by the U.S. conflict with Iran. This marks the 32nd drawdown of 5+% for U.S. stocks since March 2009 (which averages out to roughly two drawdowns per year over the past 17 years). As we like to remind clients, volatility like we’ve experienced recently is the “price of admission” for owning stocks and should be expected with regularity.

What’s Matt Reading? (March 2026)

This month, we explore the limits of historical market data, glean wisdom from a 108-year-old Wall Street veteran, and discuss why the pioneer of the ‘Yale Model’ recommends passive index funds for everyday investors.

What’s Matt Reading? (Feb 2026)

This month, we consider the optimal amount of inheritance to leave your children, the critical importance of manager selection in private markets, and how financial journalists can lead investors astray.

2025 Annual Letter

“The ultimate form of preparation is not planning for a specific scenario, but a mindset that can handle uncertainty.” – James Clear “Your family is broken but you’re going to fix the world.” – Naval Ravikant The Ceiling The main challenge of 2025 wasn’t markets, unique client situations, or asset growth. It was a founder…

Read More

What’s Matt Reading? (Jan 2026)

This month, we explore what historical agricultural data tells us about AI job displacement, why premium Swiss watchmakers intentionally limit growth, and how short sellers help keep market prices efficient.

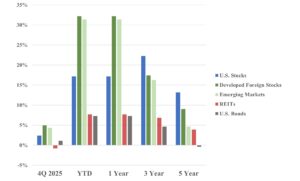

4Q 2025 Market Overview

The big story for the fourth quarter was continued strength from international stocks (in both relative and absolute terms). Developed and emerging market stock indices finished 2025 up >30% (vs. U.S. stocks up “only” 17% for the year) with help from a weakening U.S. dollar but also from a narrowing of the gap in relative valuation levels (with international stocks still trading below their historical average discount to U.S. stocks).